The Snowball Method

So you have student debt. And you are paying off a car. And you were a silly son of a bitch and didn’t read my post Credit Score which would have taught you how credit card debt builds up quickly. Now you are in debt. There are two ways to pay off debt. For more information you should check out the book I Will Teach You to be Rich by Ramit Sethi.

With the snowball method, you start by paying the minimums on all cards and loans. It will take forever if you continue to do this. The more you spend on your debt, the more money you save in the end. Credit card companies, and some banks, will charge you outrageous interest, then they will charge you the minimum monthly payment, which will be low enough that they can continue to charge you interest. Do pay the minimum monthly payment however, as your credit score will drop drastically if you do not. So the first step is to make sure you are paying the minimum payment due on all of your debt. You should be able to set up automatic payments so you don’t forget. Just set a reminder to check to make sure you have enough in your account. Once you are sure you are doing this, start making higher payments on the card or loan with the lowest balance. When this balance is completely paid off, move to the next lowest balance, and so on.

If you are the person who gets the easiest thing done on your to do list first, this method is for you. Basically, once you see a balance paid off, you realize that is possible, and the feeling of accomplishment will spur you to continue. Also paying off the lowest balance will give you access to the money you were spending in these payments quicker, to put towards the larger balances.

The Common Method

This starts the same way as the snowball method. Make sure you are paying the minimum on all balances. This is true no matter what. What makes it different, is you focus on the balance with the highest interest rate, or APR, first. If you are motivated to get out of debt and save money over time, this is for you.

This is technically better for you in the long run. If you are paying the minimum on accounts with high interest rate, you will accrue a higher balance over time. This means you will end up spending more money. So if you focus on the balance with the higher interest rate first, you will save more money over the course of paying off your debt.

It can feel a little like drowning. This is the method I use. It is hard, I am not going to lie. You are throwing money at something that is also growing. So it feels like you are throwing money away, because you are spending a lot of money, but the balance is not going down as much as you would like it to. It is saving you money over time, but it definitely doesn’t feel like it. Trust the math, and stick with it. You can do it!

How Much Do You Pay

Ok, so you are making the minimum payment on all of your debt. You have picked a method. But how much do you spend on the account you have chosen to spend more on?

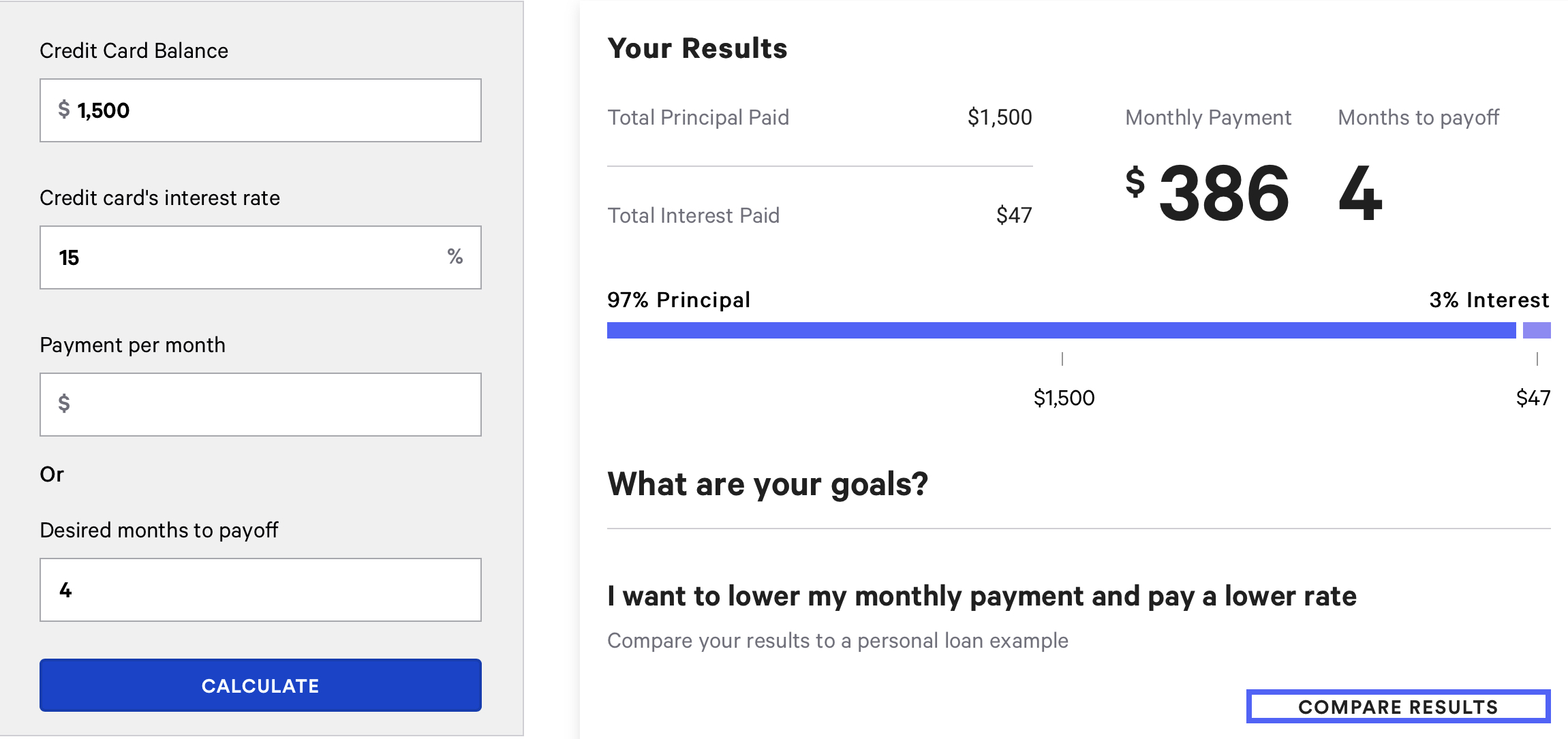

A great way to do this is to check out Bank Rate. Plug in all of the fields and play around with how much you think you can afford, and how long you want it to take to pay it off. It will be a little eye opening if you have never checked it out before.

I have brought my credit card debt down from $5000 to $1500. I started at the beginning of the year. I am going to reevaluate how much I am spending by using the Bank Rate calculator. I may be able to may less monthly and still have paid it off by the end of the year, which was my goal. If this is true, the remainder I will begin putting into my savings.

Do you have debt? How are you paying it off? Which method would you choose? Let us know in the comments below!